Good Practice Examples

Recommendations

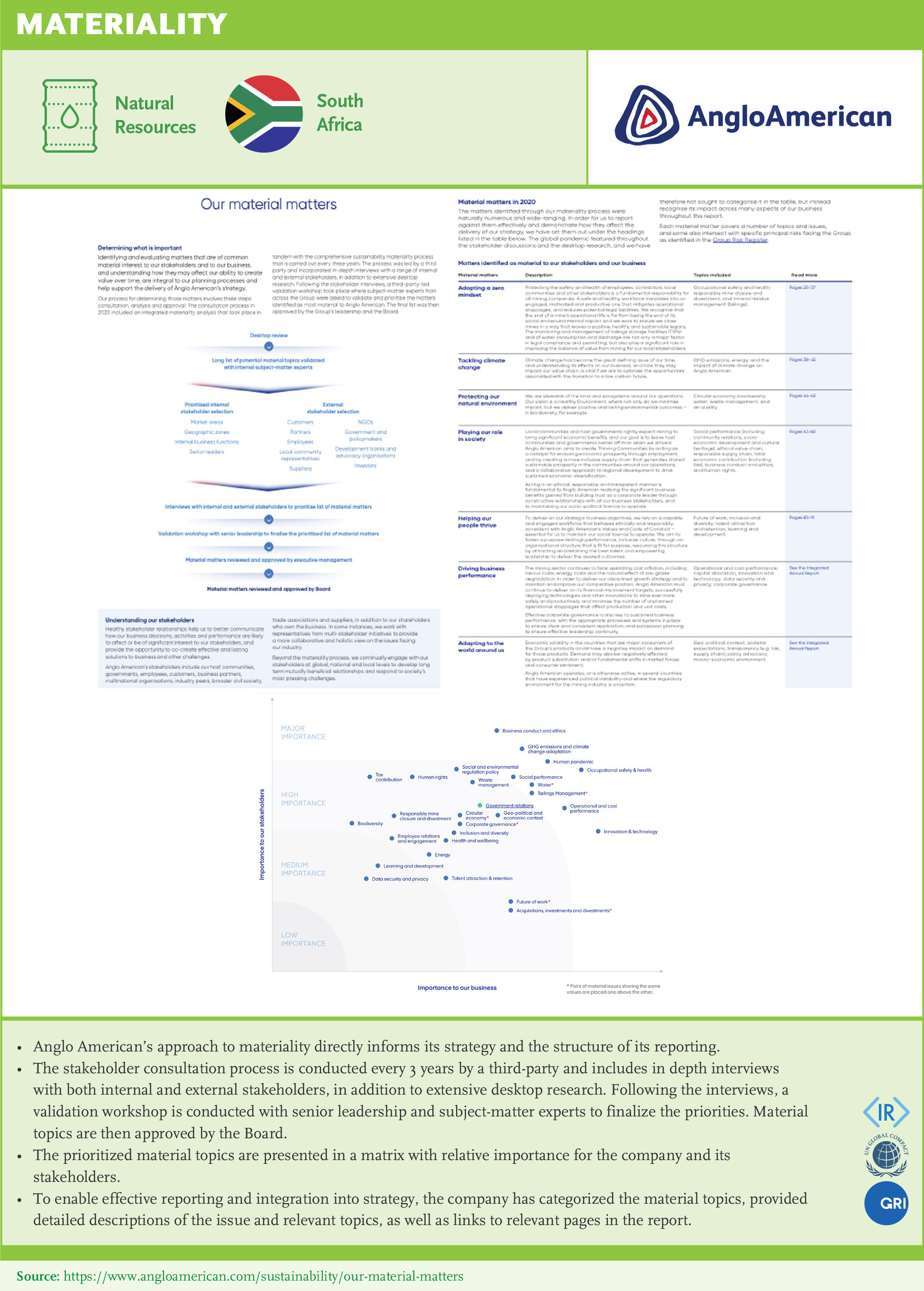

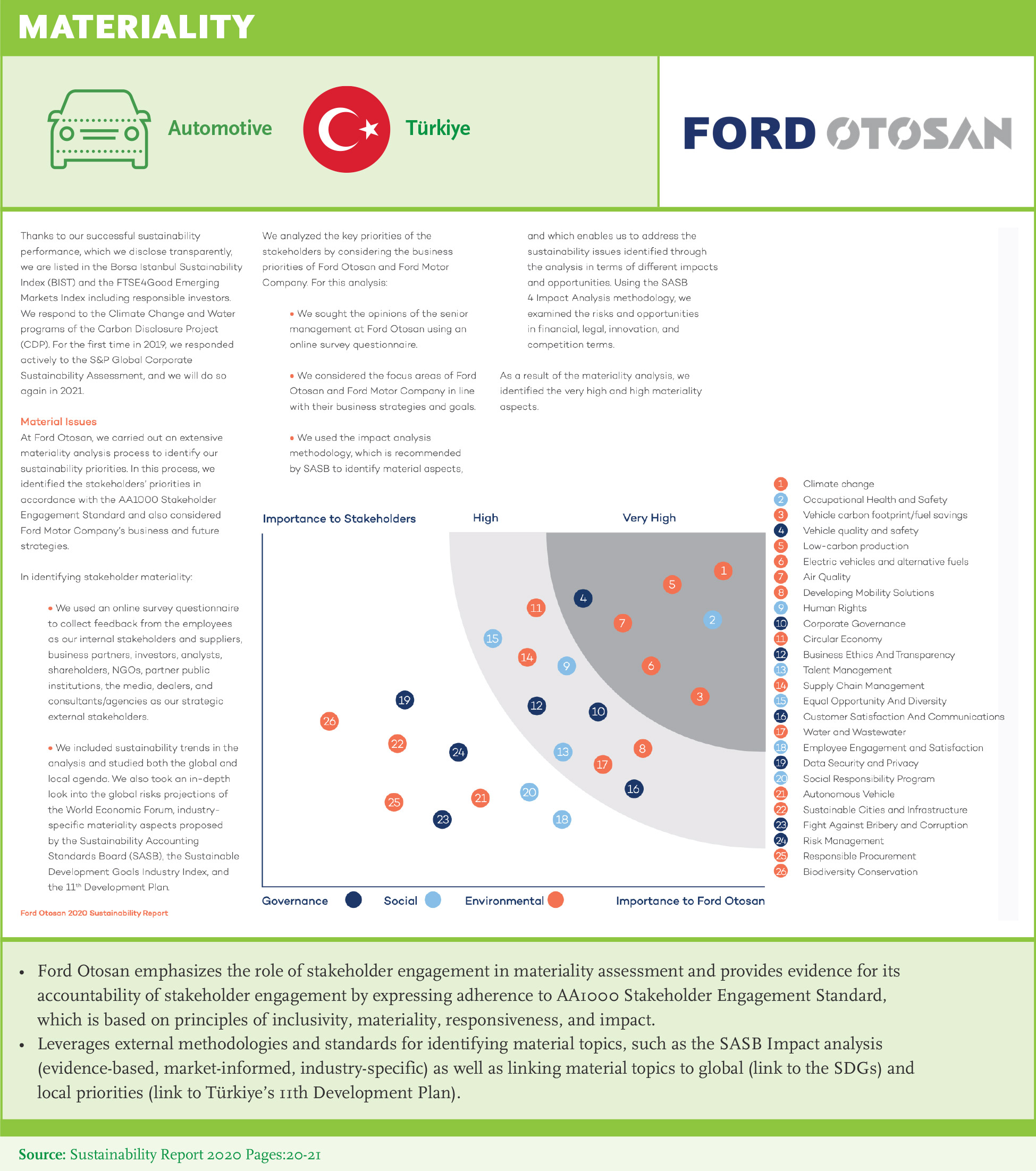

Define and engage your stakeholders: Best-in-class companies identify a comprehensive set of internal and external stakeholders and prioritize engagement based on the importance of the stakeholder for long-term value creation. Companies should deploy a variety of stakeholder engagement methods to create dialogue including one-on-one meetings and participatory tools such as focus groups to understand the stakeholder’s needs and co-create solutions.

Define material issues for each stakeholder group and how to address them: Be transparent on which topics you engage on, and how you plan to address them.

Define governance structure to support stakeholder engagement: Companies should define responsibilities, process, and information flow for stakeholder dialogue and prioritization of material issues. The boards need to understand the key issues raised by the stakeholder engagement process and how the management plans to address them. Furthermore, the board needs to have a process to evaluate the management’s sustainability plans to address the key issues.

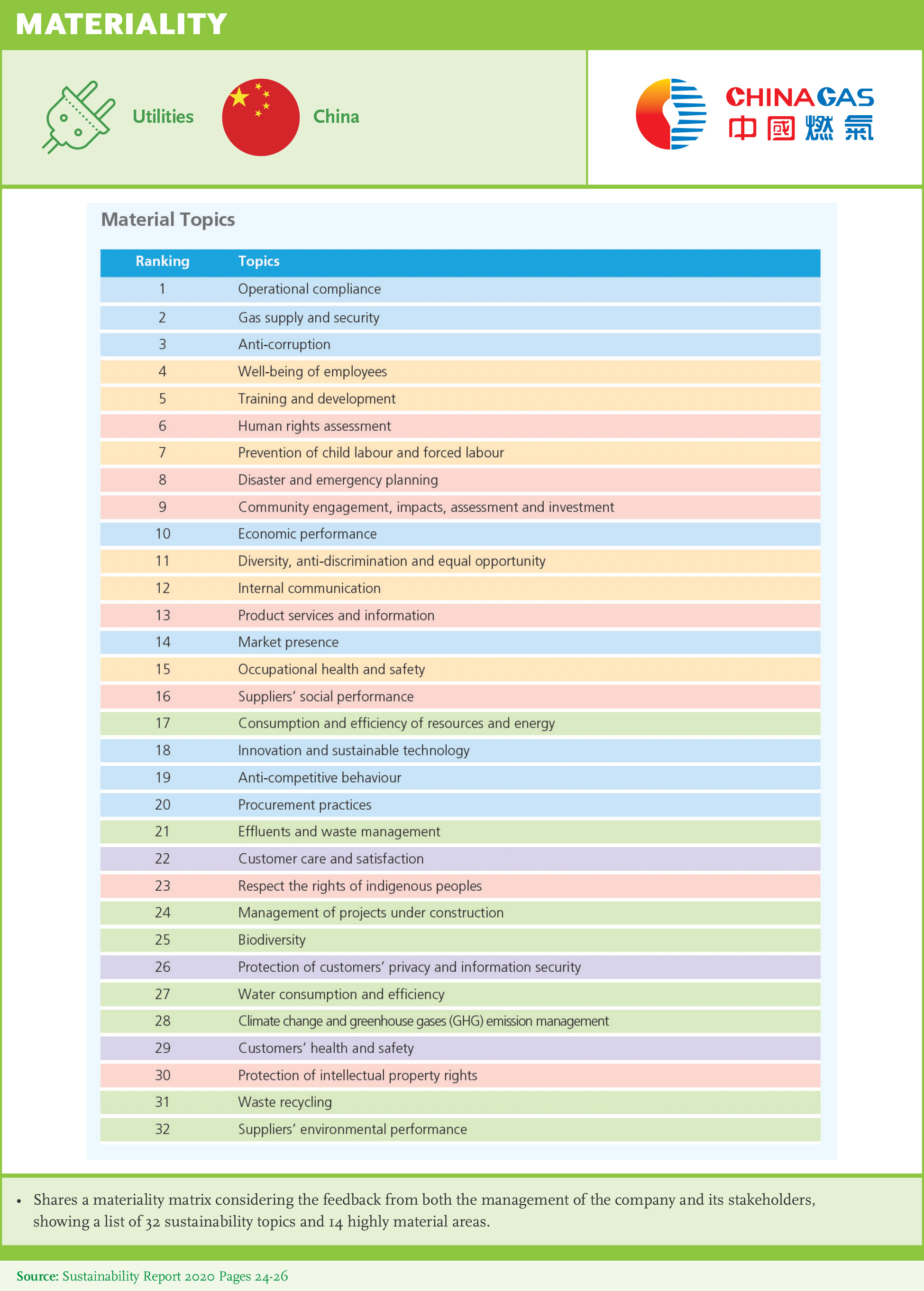

Define and prioritize material ESG topics for company and its stakeholders: Companies should define material ESG topics including risks and value creation opportunities for the company and ensure the board is involved in setting materiality thresholds. Reporting standards such as SASB and GRI can be used to identify a comprehensive list of material issues. Materiality is a function of time and audience – best practices adopt an expanded view of time to encompass long-term sustainability objectives as well as define material issues for their value chain and stakeholders. Prioritizing material issues also requires the company to evaluate its ability to influence the issue.

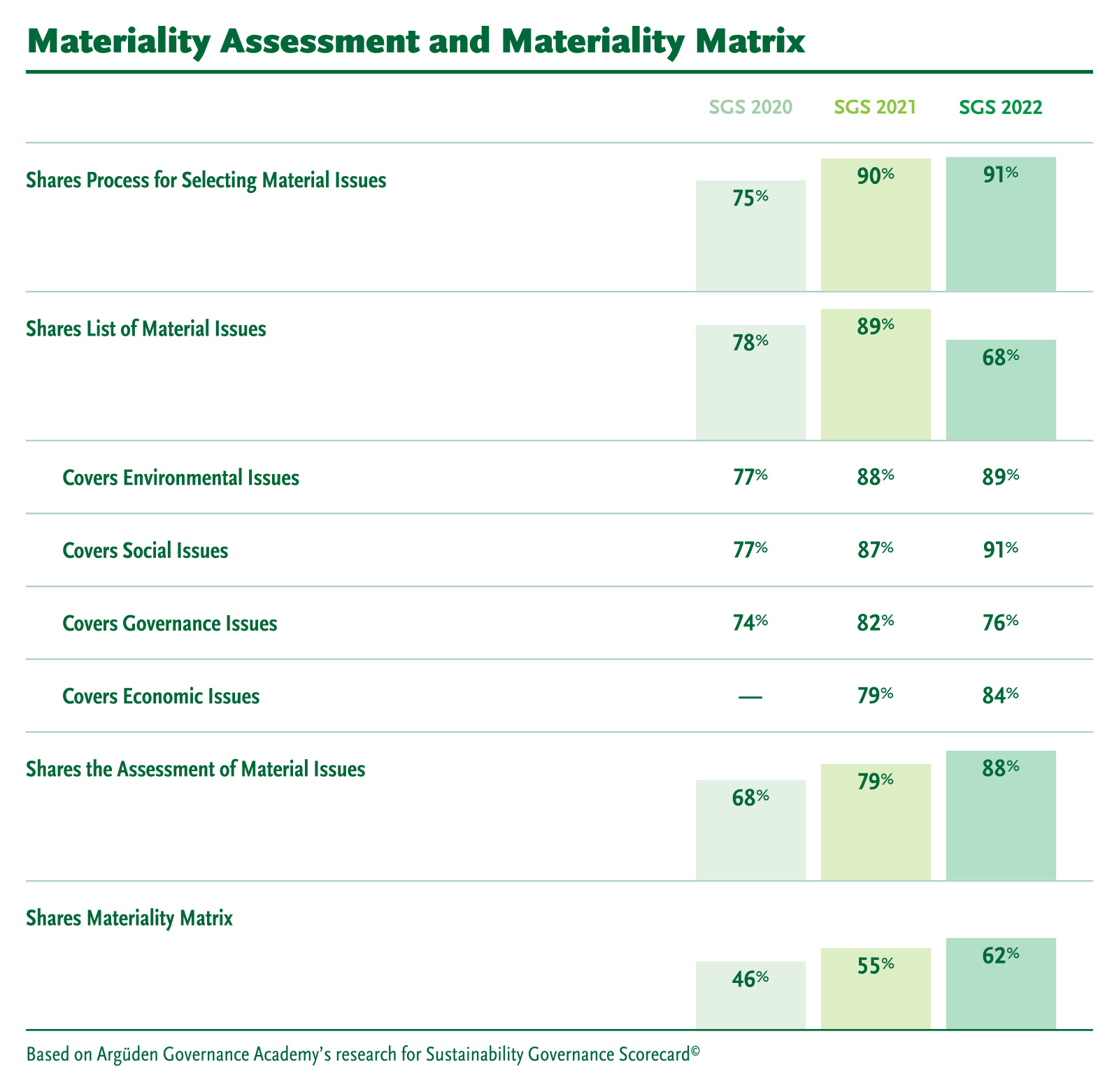

Publish a materiality matrix: A materiality matrix provides information on the most material ESG issues for the company and forms the basis of prioritization. Best-in-class companies disclose a materiality matrix that includes an assessment of materiality for the company and its stakeholders, the size of potential impact, and link with the SDGs.

Use reporting as a tool for transparency on communicating with stakeholders on what matters. Corporate reporting is a communication tool for a wide range of stakeholders. Reporting should be precise, reader friendly and provide the opportunity to assess the value created by the company. It should identify material issues relevant for different stakeholders so that it can form the basis of constructive dialogue and stakeholder engagement. Companies should clearly disclose the process for selecting material issues and the board’s role in the process.