A sustainable global economy is one that combines long term profitability with ethical behavior, social justice, and environmental care. When we look at the state of the world today – climate change, deteriorating water resources, plastic waste, income inequality, gender inequality, corruption – it is evident that institutions need to assume responsibility for sustainable development and take action.

For corporations to truly contribute to a sustainable future, there is a need to widen the lens through which we view sustainability. Sustainability requires decision-making processes that incorporate all potential impacts of a company, incorporating the positive and negative externalities into its decision-making processes, and avoiding short-sightedness and selfishness.

This means:

- Adopting a comprehensive view of how a company creates value beyond financial measures to include economic, environmental, social, and governance outcomes throughout the value chain,

- Adopting a long-term perspective and incorporating different time- horizons into the strategy and target-setting processes,

- Considering direct and indirect impacts of the company’s decisions and actions,

- Becoming more inclusive by considering the impact of all their decisions and actions on all stakeholders, current and future,

- Taking responsibility for managing and positively influencing their value-chain and ecosystem and opening to new ways of collaboration to solve sustainability challenges.

Gaining the trust of stakeholders requires transparent disclosure on all these dimensions in an integrated manner. If we expand our perspective to include all the impacts that a company creates now and in the future; we need to upgrade our measurement, evaluation, and reporting practices accordingly.

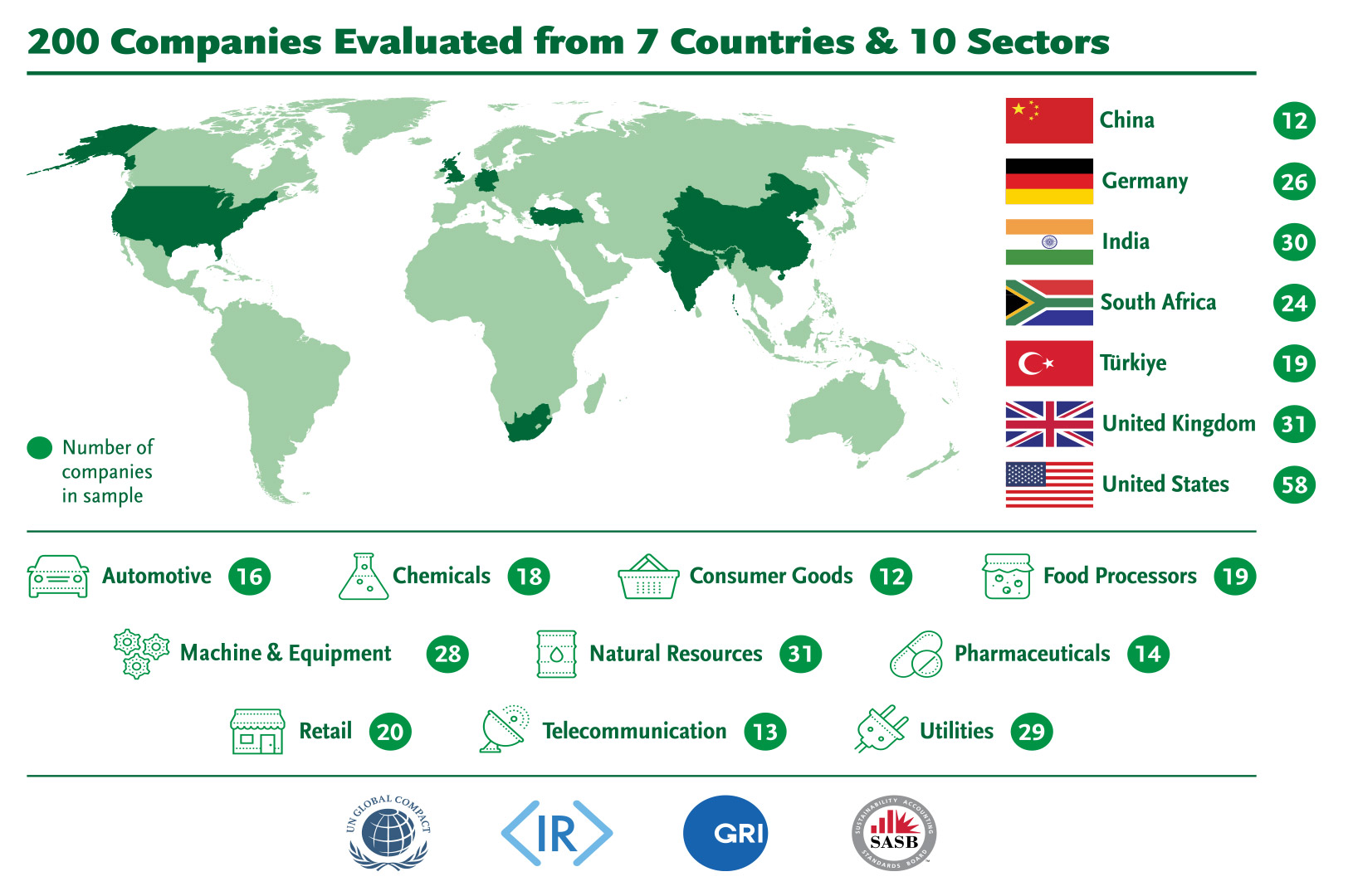

This year marks the 4th year of Sustainability Governance Scorecard – an impact-research aimed at improving the state of the world by accelerating learning from peers. Since 2019, we analyze the public disclosures of 200 Global Sustainability Leaders (GSLs) that are part of Sustainability Stock Exchanges Initiatives from 7 countries and 10 comparable sectors. We analyze annual and sustainability reports through a ‘governance lens’ to identify and share insights from the GSLs on how they provide governance to their sustainability efforts and to share best-practice examples. Below, we summarize this year’s results:

Sustainability Governance Scorecard©

Responsible Boards

Sustainability Performance

Key Conclusions

-

Build responsible boards and set up effective governance mechanisms for sustainability:

Boards set the tone at the top. Board Leadership is key for setting the company’s direction and ensuring long-term value creation for the company and its ecosystem. Responsible Boards ensure that sustainability issues are integrated into the company’s strategy and reflected in its policies and practices. This is possible through setting the right governance (guidance and oversight) mechanisms, ensuring the board has the composition and skills to lead sustainability and tying executive compensation to sustainability metrics to incentivize management towards sustainable value creation in the long run.

SKILLS MATRIX: GSLs that publish Skills Matrix increased from 26% in SGS 2019 to 60% in SGS 2022, and 48% of those included sustainability as a skill in their skill matrix.

EXECUTIVE COMPENSATION: Companies that share compensation linked to sustainability KPIs increased from 29% in SGS 2020 to 48% in SGS 2022.

BOARD GUIDANCE AND OVERSIGHT: All GSLs have adopted ESG policies in material topics. All GSLs define oversight structures & board committees to address sustainability risks and opportunities. In the last three years, some form of independent audit coverage of sustainability issues for GSLs have been around 80%, while independent audit coverage for the supply chain increased from 23% in SGS 2019 to 58% in SGS 2022.

-

Manage sustainability impact for the company, supply chain and ecosystem through rigorous target- setting and transparency on performance:

What gets measured gets improved. There is a need to move beyond checking boxes and marketing material to embedding ESG considerations into strategy and operations. Reporting should cover material ESG areas and provide evidence on targets, results, and evaluation of results to signify a learning loop (including trends, benchmarks). There should be a mindset shift towards looking at the whole (short-term, long-term, all relevant ESG issues, supply chain and ecosystem, individual and global goals) rather than just reporting on parts. The scope of reporting should be comprehensive and include all employees, geographies, supply chain and the ecosystem. This requires more rigorous target-setting and measurement of material issues by companies, regular feedback from investors on what matters for decision-making and unification of reporting frameworks, at least at the sector-level.

KPIs, TARGETS, RESULTS, RESULTS EVALUATION: As part of our research, we evaluated whether a company sets policy, KPIs and targets and shares results and evaluation of results across specific ESG categories. We find that >98% of GSLs report results on Environmental, Social and Governance Topics, while there is need for more rigorous target setting. 87% of GSLs set targets for environmental topics (primarily climate change, significant room for improvement for other categories such as water, waste, biodiversity), 82% for governance (primarily executive compensation), and 66% for social sustainability issues (<50% for all sub-topics including Diversity and Health & Safety).

RESULTS COVERAGE: Managing sustainability requires a company to assume responsibility to manage the impact of all its activities, including its supply chain and the full product portfolio throughout the lifecycle of its products. Among the GSLs, 87% share sustainability targets for the business (compared to 76% in SGS 2020), while only 40% share targets for their supply chain (compared to 29% in SGS 2020).

SUSTAINABILITY STEWARDSHIP: Increasingly, companies must assume responsibility not just for the impact of their own operations but also manage their ecosystem if they are to thrive in the long-run. Strategy alignment with Sustainable Development Goals has increased from 73% in SGS 2020 to 88% in SGS 2022, and results sharing linked to SDGs has increased from 58% to 82%. Aligning incentives with the world we want in the future requires changes in the system. For this, Global Sustainability Leaders need to take leadership to act fast and scale-up progress. If we are to reach the global goals in 2030, companies should step-up to set targets, measure outcomes and partner for scale-up. We find that only 57% of GSLs set targets for the SDGs in SGS 2022, a slight increase from 50% in SGS 2021.

-

Craft a purpose-driven, stakeholder-centric model for managing sustainability and adopt continuous improvement as a mindset through the sustainability journey:

License to operate in today’s world requires responsible leadership – companies who actively manage sustainability will be of benefit to both the company and the society. Reaching the SDGs requires setting-up a multi-layer multi-year process and requires cooperation from stakeholders. When crafting the sustainability approach, companies must move to a more stakeholder-centric model and widen their view to encompass their ecosystem and long-term impact.

VALUE CREATION MODEL AND PURPOSE: Best-in-class companies identify a corporate purpose that encompasses sustainability goals and build a culture around it. A clear statement of purpose unites executives, directors and investors on the company’s priorities and creates the link between strategy and capital allocation decisions. We find that 65% of GSLs show a visual and holistic value creation model. Best examples of holistic thinking on value creation are found in companies that embrace Integrated Reporting.

STAKEHOLDER ENGAGEMENT AND MATERIALITY: Engaging stakeholders is key to obtaining the social license to operate in the 21st century. Best-in-class companies adopt a long-term comprehensive view of their stakeholders to encompass external stakeholders (environment, supply chain, communities), and engage their stakeholders to identify material ESG issues. Publishing a materiality matrix including assessment of materiality for the company as well as its stakeholders, is a good communication tool to align management, investors, and other stakeholders on what matters in the short-term and the long-term. Whereas only 46% of GSLs published a materiality matrix in SGS 2020, 62% of GSLs shared a materiality matrix in SGS 2022.

SUPPLY CHAIN SUSTAINABILITY: Many companies’ greatest sustainability risks and opportunities are in their supply chain. As a result, companies must set standards, manage risks, and invest in the development of their supply chains for a step-change in sustainability impact. This may involve utilizing their purchasing power to encourage, audit, collaborate with and provide benchmarking, and learning opportunities with its suppliers on key sustainability issues. Coverage of sustainability issues in the supplier assurance process increased from 75% in SGS 2020 to 85% in SGS 2022, and supply chain assurance results disclosure on sustainability increased from 43% in SGS 2020 to 61% in SGS 2022. Although there is progress, there is clearly room for more rigorous audit and more transparency.

LEARNING AND DEVELOPMENT: Sustainability is a continuous journey. To ensure progress is sustained over the long-run, companies must establish a learning loop for continuous improvement and create a climate of learning with measurable indicators (trends, benchmarking). Lessons learned should be utilized to improve decision-making processes, skill gaps and required mindset changes need to be addressed through training, and sustainability practices need to be integrated into the company’s processes. Furthermore, development training and development opportunities should cover employees in all geographies, supply chain and communities. 96% of GSLs reported conducting social sustainability training in SGS 2022 (mostly Health & Safety, Talent Development and Diversity training) and 78% reported governance training (mostly compliance-related). Less than half of all GSLs reported conducting environmental sustainability training (<20% of GSLs reported training on any environmental subtopic including climate change).